The thesis

The sky is no longer safe. A drone small enough to fit in a backpack, cheap enough to buy online, can slip past radar, evade jamming, and deliver a payload with pinpoint precision. Militaries that spent decades building billion-dollar missile defence systems are watching those systems fail against a ten-thousand-dollar commercial drone. The question isn't whether the world needs counter-drone technology. The question is who actually controls it.

The answer isn't Lockheed Martin. It isn't Raytheon. It's a company that most investors have never heard of — that Lockheed Martin just came to, because Lockheed needed what they have. The ticker is ONDS. And it isn't a drone company. It is building the operating system for autonomous warfare and critical infrastructure intelligence.

Key numbers

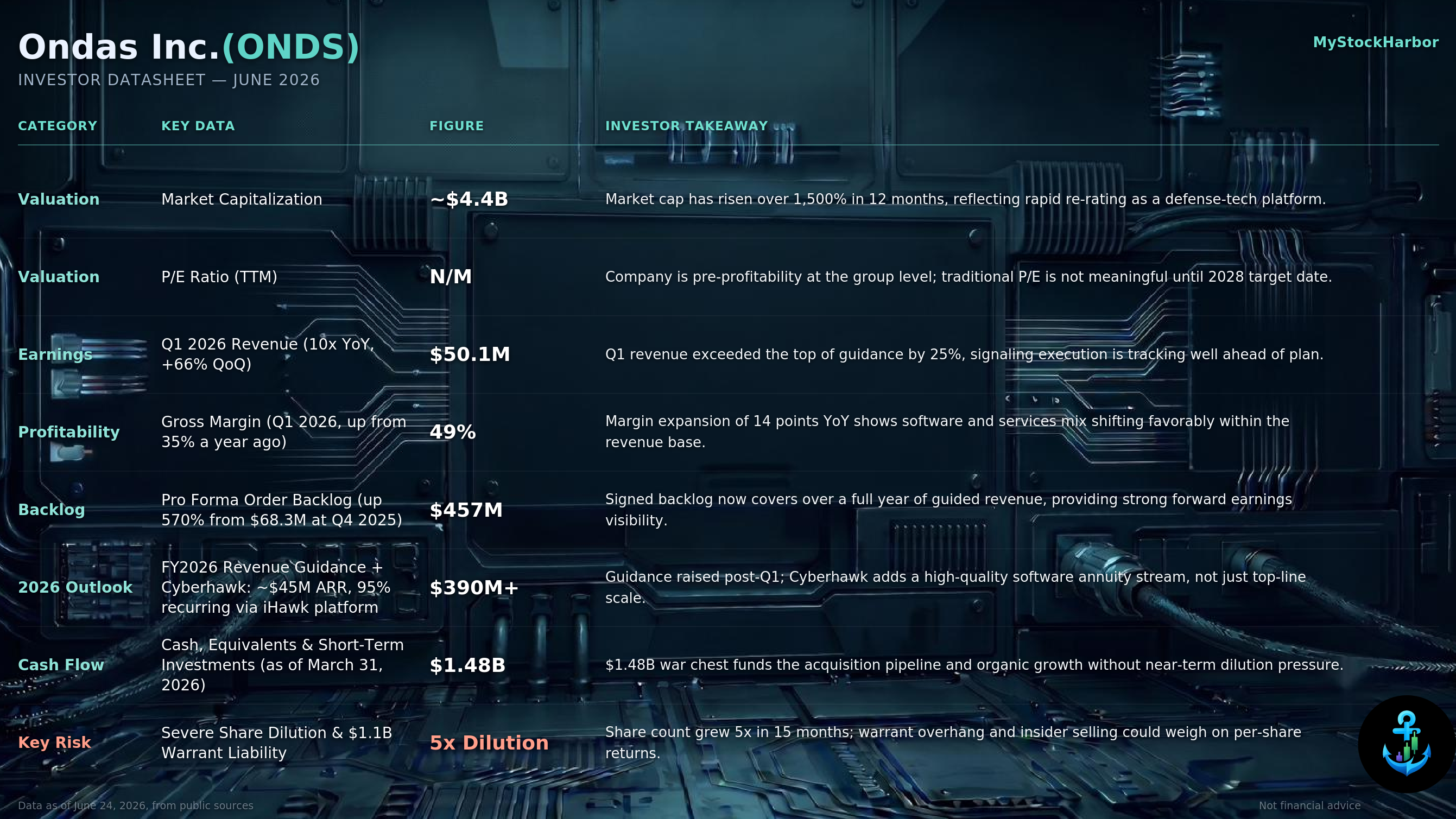

- $457M pro forma backlog — up from $68M at end of 2025, a 570% surge; signed backlog now covers over a full year of guided revenue, providing strong forward earnings visibility

- $50.1M Q1 2026 revenue — ten times what it was a year earlier; exceeded the top of guidance by 25%, signalling execution tracking well ahead of plan

- 49% gross margin in Q1 2026 — expanded 14 points year-over-year from 35% as software and services increasingly dominate the revenue mix

- $390M+ full-year 2026 guidance — raised post-Q1; Cyberhawk adds a high-quality software annuity stream via iHawk (~$45M ARR, 95% recurring), not just top-line scale

- $1.48B cash and short-term investments — war chest funds the acquisition pipeline and organic growth without near-term dilution pressure; profitability target Q1 2028

- ~$4.4B market cap, P/E N/M — market cap risen over 1,500% in 12 months reflecting rapid re-rating as a defence-tech platform; traditional P/E not meaningful until 2028 target date

The setup

Sentrycs is the keystone technology — and it does something no kinetic or jamming system can. Every commercial drone maintains a radio link to its controller following a communication protocol. Sentrycs reads that protocol, interprets the command structure, and inserts its own commands in real time. It doesn't block the signal. It becomes the signal. Then it orders the drone to land. A swarm of twenty drones approaching a military base: a kinetic system engages each one individually with explosions and shrapnel risk; a jamming system blacks out every wireless communication in the area including your own. Sentrycs takes control of each drone, guides it to a safe landing zone, and preserves every friendly frequency in the process.

This is why Lockheed Martin didn't build this themselves — it requires deep simultaneous expertise in wireless communication protocols, RF signal analysis, and real-time AI inference. That is not a missile defence company's core competency. It is Ondas'. Lockheed integrated Sentrycs directly into its next-generation Sanctum C-UAS platform. No Ondas, no Sanctum, no Lockheed C-UAS integration. Every Sanctum contract is now a Sentrycs contract — and Lockheed has a very long order book.

Beyond Sentrycs, Ondas has built an entire autonomous systems stack: American Robotics for industrial rail and infrastructure drone inspection, Airobotics for ports and border security, World View Enterprises for balloon-based stratospheric surveillance at 100,000 feet for the US Navy, and Cyberhawk — an AI-enabled infrastructure analytics platform generating over $45M in annual recurring revenue via the iHawk software platform. Ground, air, stratosphere, software. That is not something a competitor builds in two years.

Risk factors

- Share dilution is the single biggest overhang: Share count grew five times in fifteen months, with a $1.1B warrant liability. Warrant overhang and insider selling could weigh on per-share returns regardless of underlying platform performance.

- Pre-profitability at group level: Despite expanding gross margins and strong unit economics, the company is not yet profitable. The Q1 2028 profitability target is a long runway, and any execution miss extends the loss period.

- Acquisition integration complexity: Sentrycs, American Robotics, Airobotics, World View, and Cyberhawk all acquired in rapid succession. Integrating these into a coherent operating platform at pace is a significant management execution challenge.

- Backlog conversion risk: Pro forma backlog of $457M includes newly acquired businesses. The key question is how much converts to recognised revenue on schedule and at the guided gross margin.

What to watch

The Cyberhawk acquisition closing is the near-term catalyst — it cements the software annuity revenue into the books and opens the platform to every major energy and telecoms operator running infrastructure inspection globally. Watch for Sanctum contract announcements from NATO-aligned militaries, since each one is a direct Sentrycs revenue event. The LADOS platform — unveiled at Eurosatory 2026 — is the longer-term watch: if Layered Autonomous Defence Operating System gains traction as a unified autonomous command structure integrating loitering munitions, C-UAS, and ground robotics, it repositions Ondas from a component supplier to the operating system of autonomous first contact. The retail crowd is looking for the next drone play. The institutional question is different: who controls the software layer of autonomous defence?