The thesis

A single missile interceptor can cost more than two million dollars. The drone it's trying to shoot down can cost less than a used car. Fire enough of those and you don't lose the war — you go broke winning it. That is the arithmetic underneath every modern conflict right now, from Ukraine to the Red Sea to the Pacific: nobody is fighting for one decisive battle anymore, they're fighting a war of production, and the side that can lose the most, the cheapest, the fastest wins before the expensive side even runs out of courage.

Most investors think the winner of the drone era will be whichever prime contractor builds the most advanced next-generation fighter. They're wrong. The winner is whoever builds the thing that gets shot at instead — cheap enough to mass-produce, expendable enough to lose on purpose, and available in numbers the exquisite jet can never match. The ticker is KTOS. Kratos Defense & Security Solutions doesn't try to out-build Lockheed Martin or Northrop Grumman, and it never bids to be the prime contractor holding the multi-billion-dollar program of record. It builds the parts of the kill chain that need to be cheap, fast, and disposable — the parts every prime, on every platform, eventually needs and can't build fast enough itself.

Key numbers

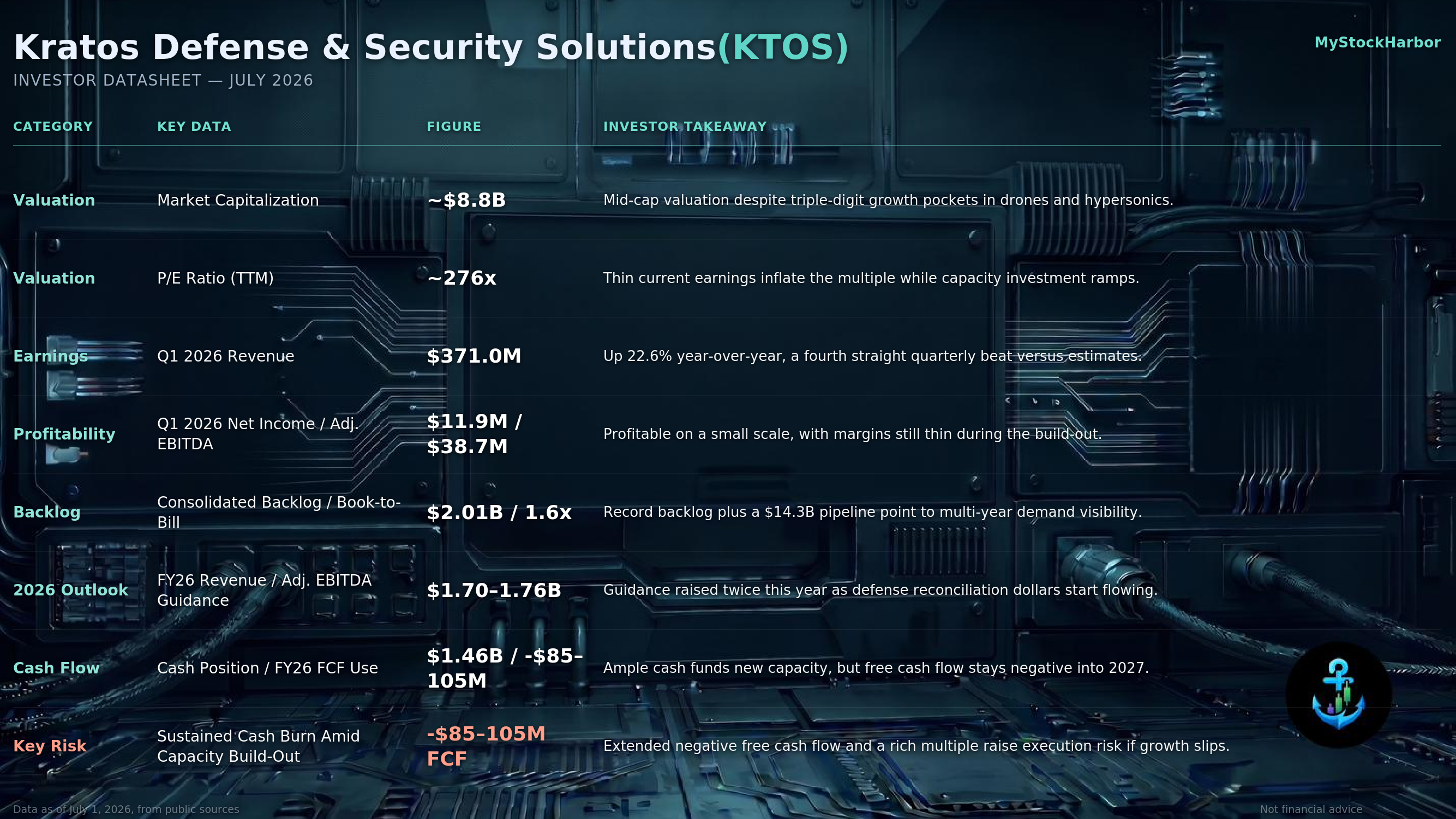

- $2.01B consolidated backlog, 1.6x book-to-bill — plus a bid-and-proposal pipeline above $14.3B, more than eight times FY26 guided revenue; management called it the largest backlog in company history

- $371.0M Q1 2026 revenue — up 22.6% year-over-year, a fourth consecutive quarterly beat against estimates

- $11.9M Q1 2026 net income / $38.7M Adj. EBITDA — profitable at a small scale, with margins still thin during the capacity build-out

- $1.70-1.76B FY26 revenue / Adj. EBITDA guidance — raised twice this year as defense reconciliation dollars start flowing

- $1.46B cash position vs. -$85M to -$105M guided FY26 free cash flow — ample liquidity funds new factories and test facilities, but free cash flow stays negative into 2027

- ~$8.8B market cap at a ~276x trailing P/E — thin current earnings inflate the multiple while the company invests ahead of revenue

The setup

Start with the aircraft: Kratos builds the XQ-58A Valkyrie, a jet-powered "loyal wingman" drone that flies alongside a manned fighter — it scouts the threat, draws the fire, and if it gets shot down, nobody writes a letter to a family. Almost nobody else can build it at the same cost and pace, because the capability didn't start with Valkyrie. Kratos spent roughly three decades building the aerial target drones the U.S. military uses to train its own pilots and missile defenses — thousands of low-cost, jet-powered airframes engineered to be shot down on purpose. That target-drone business quietly became the wartime factory: the same cheap jet engines, disposable airframes, and fast production lines the entire drone-warfare era now needs at scale.

The second bottleneck is less visible and more physical. Hypersonic missiles get talked about as a materials-and-aerodynamics problem, but the real constraint is manufacturing: someone has to produce the solid rocket motor that gets the missile moving, at a scale the U.S. industrial base largely stopped building for decades. Kratos is one of the only American companies still producing solid rocket motors and hypersonic test systems at meaningful volume, and it just broke ground on a new hypersonic test facility in Odon, Indiana, built to keep pace with a Pentagon that wants this capability now. Kratos also doesn't compete with the primes — it sells to nearly all of them. It's partnered with Airbus on unmanned systems and integrated its own J85 engine into the Army's Firejet drone program, proof the model works across more than one customer at a time.

Risk factors

- Negative free cash flow: FY26 FCF is guided to -$85M to -$105M as the company builds capacity ahead of revenue — a real risk if defense spending or program timing cools

- Rich valuation: a ~276x trailing P/E prices in a lot of future execution; any guidance miss could compress the multiple sharply

- Execution and ramp risk: converting the record backlog into revenue depends on hitting build-outs like the Odon test facility and the Valkyrie production scale-up on schedule

- Budget and policy dependency: revenue is concentrated in Pentagon and prime-contractor programs, so shifts in defense budgets or program cancellations could slow new bookings

What to watch

The Odon, Indiana hypersonic test facility becoming operational is the near-term catalyst to track. Watch Valkyrie production scale roughly five-fold, from about eight aircraft a year today to a targeted forty a year by late 2027 — the clearest signal that loyal-wingman drones are moving from prototype to program of record. The June 2026 expansion of Spartan turbojet engine production for missiles and loitering munitions is a third product line riding the same disposable-hardware thesis. The market has punished Kratos on nearly every earnings report this year because the free cash flow line is red — but the backlog, the book-to-bill, and a bid pipeline eight times the size of the company say the Pentagon has already decided: the next war gets fought with expendable hardware, not just exquisite hardware.