The thesis

AST SpaceMobile isn't a satellite story, it's a mobile network story being built 500 kilometres above the Earth. The company's BlueBird satellites connect directly to standard, unmodified smartphones using the same spectrum bands carriers already operate on, turning constellation deployment into the bottleneck for global cellular coverage rather than any unproven technology. With contracts already signed and a fully-funded buildout in progress, the market is pricing in execution risk on a roadmap that's increasingly backed by hardware in orbit rather than promises.

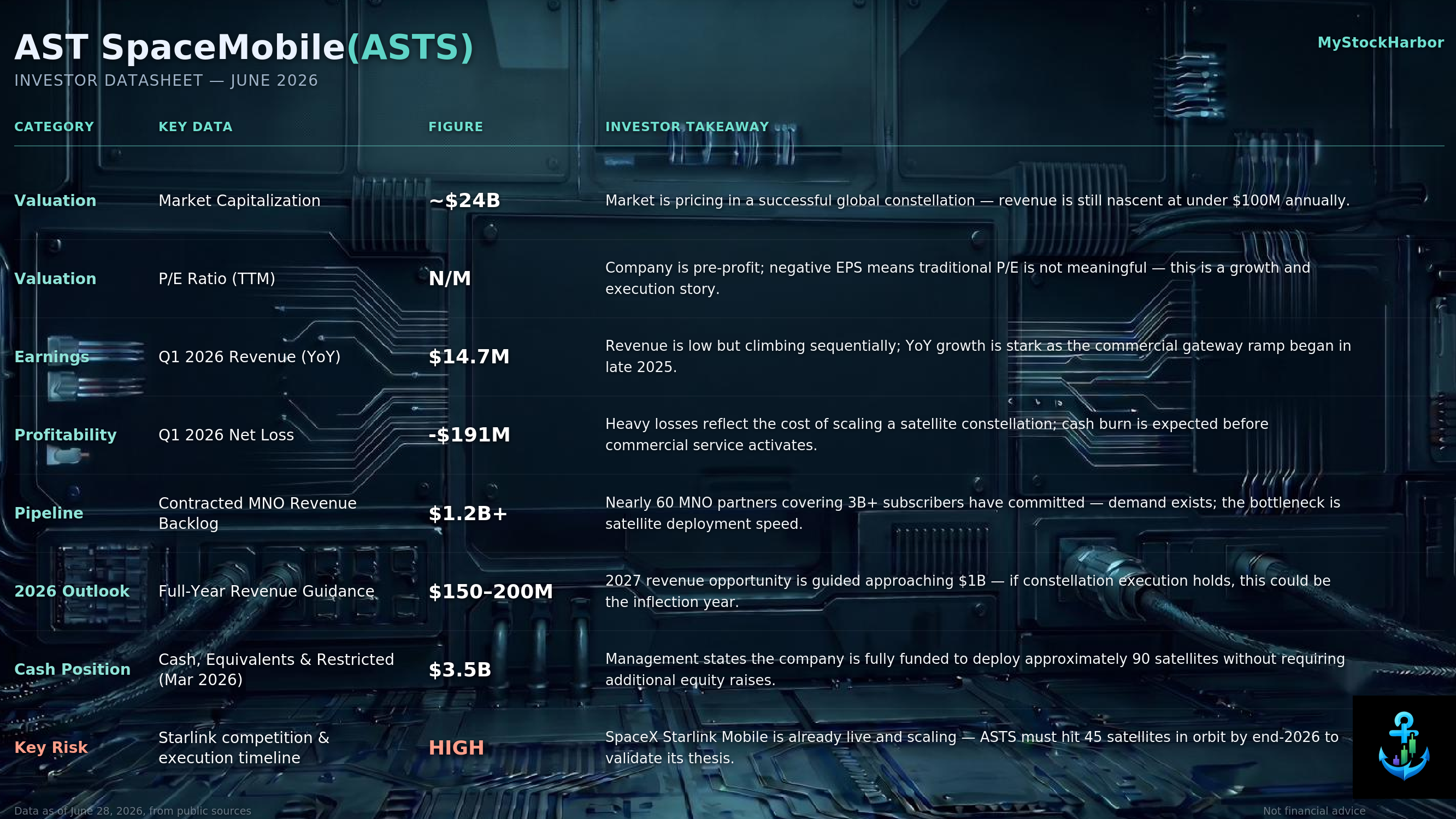

Key numbers

- Over $1.2 billion in contracted revenue commitments from nearly 60 mobile network operator partners covering more than 3 billion subscribers

- Q1 2026 revenue of $14.7 million, with full-year guidance of $150-200 million as gateway and milestone timing shifts resolve through the year

- 2027 revenue opportunity approaching $1 billion, with the majority either long-term contracted or described as highly recurring

- Approximately $3.5 billion in cash, cash equivalents, and restricted cash as of March 31, 2026, stated by management as sufficient to fund roughly 90 BlueBird satellites without an equity raise

- Approximately 3,900 patent and patent-pending claims covering the direct-to-device space-based cellular architecture

The setup

The near-term catalyst is satellite count, not earnings. Management's target is 45 BlueBird satellites in orbit by the end of 2026, the threshold for non-continuous SpaceMobile Service across key markets, with 60 satellites enabling continuous coverage in the highest-value regions. On June 17, 2026, a Falcon 9 launch added BlueBird 8, 9, and 10, all Block 2 craft, continuing a launch cadence of roughly every one to two months. The Texas manufacturing facility is reportedly producing enough capacity to support over ten satellites a month, and the FCC has already granted Supplemental Coverage from Space authorization for a network of up to 248 satellites in the US.

Risk factors

- Short interest sits above 13%, reflecting real skepticism about execution risk on the satellite deployment timeline

- Q1 2026 revenue came in well below analyst estimates, with management attributing it to shifted gateway deliveries and government milestone timing rather than demand

- The company remains pre-revenue at meaningful scale and is not yet profitable, with the investment case dependent on hitting deployment milestones on schedule

- Starlink Direct-to-Cell is already live and scaling, meaning ASTS is not the only satellite-to-unmodified-smartphone network in the market; the differentiator management leans on is true broadband-level speeds rather than the absence of hardware modifications

What to watch

The 45-satellite milestone by the end of 2026 is the clearest near-term marker of whether the deployment roadmap is on track. Beyond the consumer network, AST's government and defence subsidiary is pursuing programmes connected to the Space Development Agency and the Missile Defense Agency's SHIELD Program, which management has described as a potential multi-billion-dollar annual opportunity in aggregate over the medium term and a dimension of the story that isn't yet reflected in current revenue.